Payroll compliance India is no longer just a finance team responsibility.

Since 21 November 2025, India’s four new Labour Codes have fundamentally changed how wages are defined, how PF and gratuity are calculated, and how quickly employees must be paid on exit. If your payroll team is still running the same salary structure it used last financial year, it is running a non-compliant structure right now.

The problem most organisations face is not awareness. It is action. HR and finance teams know something has changed, but internal approvals, system upgrades, and competing priorities keep pushing the restructuring back. That delay has a direct cost. Every month without a restructured payroll is a month of compounding non-compliance.

This article explains exactly what has changed in your payroll numbers, why those changes matter operationally, and what your finance and HR teams must do to correct them.

The short version

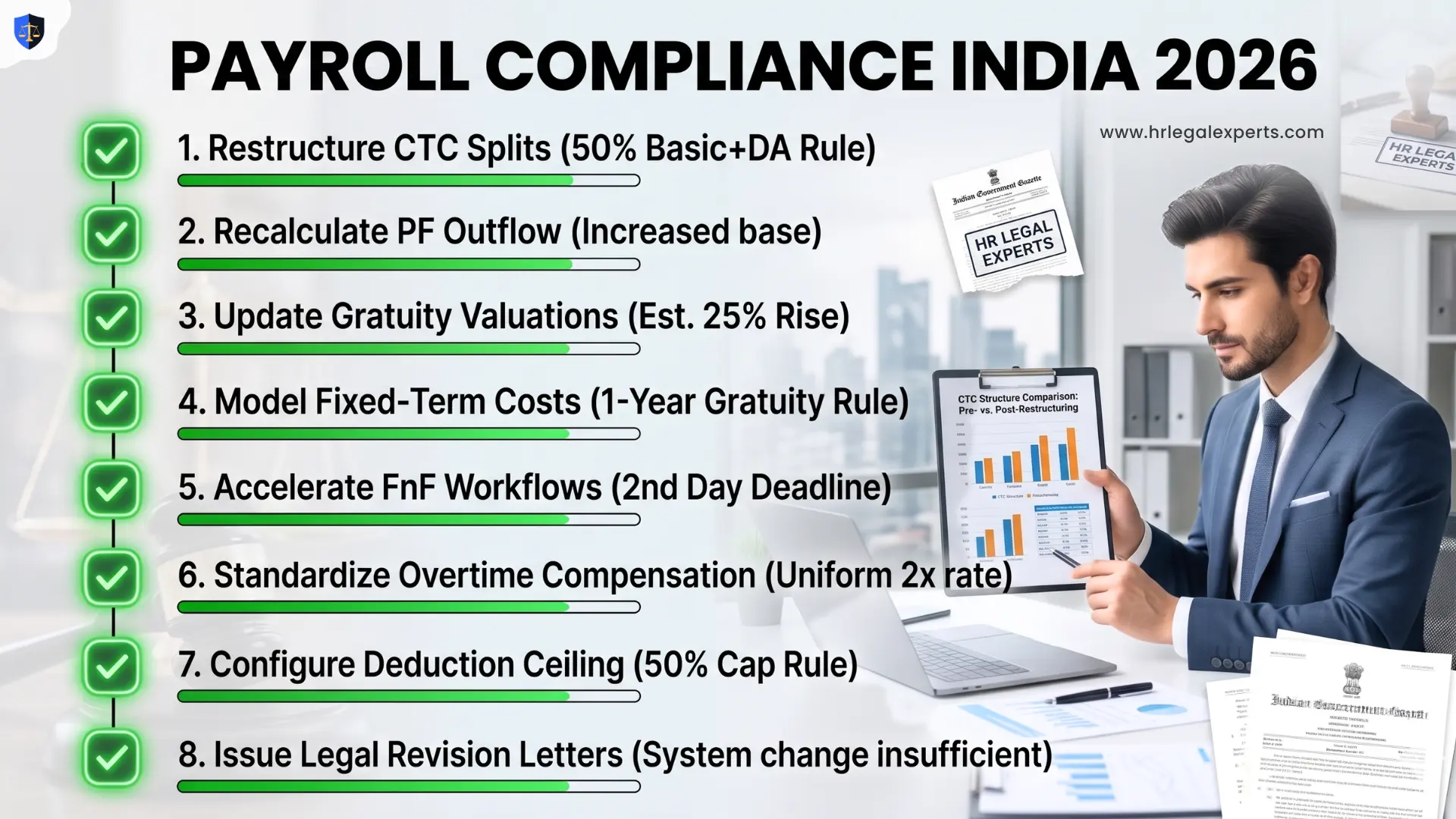

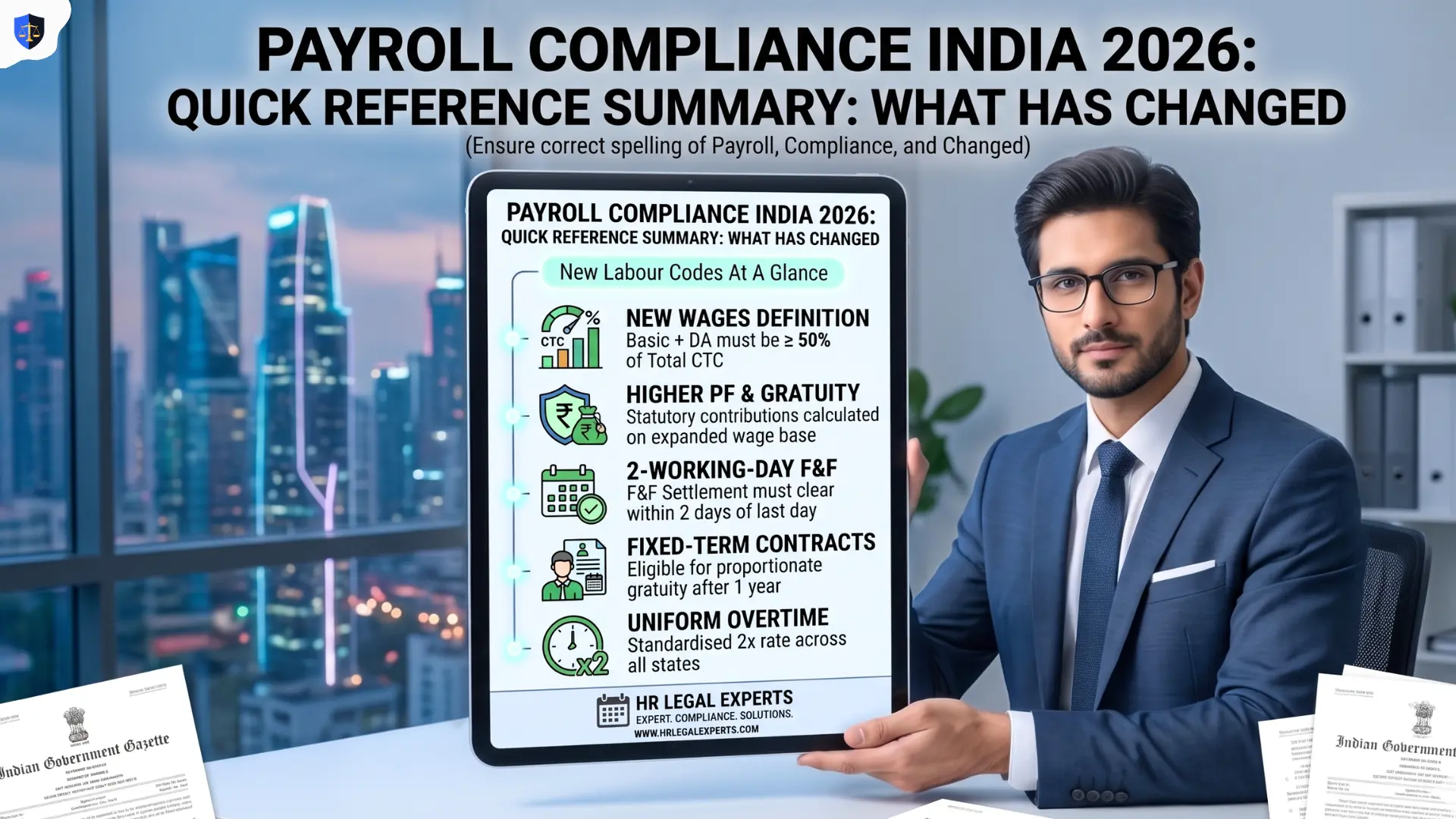

• Four Labour Codes replaced 29 central labour laws, effective 21 November 2025

• Basic salary plus DA must now be at least 50% of total CTC under the Code on Wages, 2019

• PF contributions increase for both employer and employee as a direct result

• Gratuity liability is estimated to rise by approximately 25% across organisations

• Full and Final Settlement must clear within 2 working days of last working day

• Overtime is now uniformly 2x normal wages, no state variation

• Total deductions in any wage period cannot exceed 50% of wages

New wages definition: where payroll compliance India starts

Before the new codes, India had no single, uniform definition of wages. Different Acts used different definitions, which gave companies room to keep basic salary artificially low, typically 30 to 40% of total CTC, while loading up allowances. That structure kept PF and gratuity liability down. It was common practice, and it was exactly the outcome employers intended.

The Code on Wages, 2019 eliminates that flexibility entirely. It introduces one binding definition of wages, applicable uniformly across every statutory calculation including PF, ESI, gratuity, overtime, and bonus. For a broader overview of how all four codes interact with your HR structure, the labour codes compliance guide covers the full picture.

Under this definition:

• Wages include: basic pay, dearness allowance, and retaining allowance

• Excluded components such as HRA, bonuses, overtime, commissions, and other allowances cannot collectively exceed 50% of total CTC

• Where excluded components cross 50% of total CTC, the excess is automatically reclassified as wages for all statutory purposes

In plain terms, basic pay plus DA must form at least 50% of every employee’s total CTC. There are no exceptions based on industry, headcount, or designation.

When we audit CTC structures, the breach almost always sits in the special allowance line, not HRA. That is where to look first.

Key fact: Under the Code on Wages, 2019, basic salary plus DA must be at or above 50% of total CTC. Any shortfall triggers automatic reclassification of excess allowances as wages, which increases PF, gratuity, overtime, and bonus liability simultaneously.

How the new wages rule changes your payroll numbers

1. PF contributions rise on both sides

Provident Fund contributions are calculated on wages as defined under the EPF and MP Act, 1952. Because wages now include a structurally higher basic salary component, both employer and employee PF contributions rise proportionally and immediately.

Consider an employee earning Rs 10 lakh annual CTC. Under the old structure, basic pay was commonly set at Rs 3.5 lakh, which is 35% of CTC. That produced an annual employer PF contribution of Rs 42,000. Under the revised structure, basic must be at least Rs 5 lakh, which is 50% of CTC. That takes the annual employer PF contribution to Rs 60,000. The difference is Rs 18,000 per employee, per year, purely from restructuring.

Multiply that by your headcount. For a company with 50 employees averaging Rs 10 lakh CTC, the additional annual PF outflow from restructuring alone can exceed Rs 9 lakh. This is not a contingent future liability. It has been a current one since 21 November 2025.

Key fact: For a 50-person company averaging Rs 10 lakh CTC, additional PF outflow from the Code on Wages, 2019 restructuring alone can exceed Rs 9 lakh annually. Organisations that have not recalculated are carrying an understated payroll liability.

3. Income tax exposure most HR teams miss

When basic salary rises to meet the 50% threshold, components that previously attracted partial tax exemptions, such as conveyance allowance and special allowance, get reclassified as wages. As a result, the employee’s taxable income often increases even where gross CTC stays completely unchanged.

Under Section 15 of the Income-tax Act, 1961, salary income is fully taxable unless a specific statutory exemption applies. Many of the allowances being restructured lose that exemption once reclassified. Employees who see a lower net salary after restructuring will ask questions. Having a clear, written explanation ready before the change takes effect is an employee relations obligation, not just an administrative nicety.

Key fact: CTC restructuring under payroll compliance India requirements can increase employee taxable income under Section 15 of the Income-tax Act, 1961, even when gross CTC is unchanged. Communicate this before the first revised payslip, not after.

4. Full and final settlement: 2 working days, hard deadline

The Code on Wages, 2019 replaces the Payment of Wages Act, 1936 and introduces a non-negotiable two-working-day deadline for Full and Final Settlement from the employee’s last working day. This applies to resignations, terminations, retrenchments, and closures equally.

Most payroll teams run on monthly cycles. An employee exiting mid-month needs an off-cycle FnF run to meet this statutory requirement. If your payroll system, approval chain, or finance workflow cannot accommodate that, you are structurally non-compliant regardless of intent.

This is an operational problem first and a legal one second. The solution is redesigning your FnF approval workflow — identifying which signoffs can be pre-authorised and which are creating delays. For the exit documentation side of this, our exit and separation templates give you a legally updated starting point.

Key fact: Under the Code on Wages, 2019, FnF delayed beyond 2 working days is a statutory violation from day three. Employees can immediately file a formal complaint through the new digitised grievance system. A monthly payroll cycle does not exempt an employer from this requirement.

5. Overtime is now 2x across every sector

The Code on Wages, 2019 standardises overtime compensation at twice the normal wage rate across all establishments. Under the Factories Act, 1948, and various state Shops and Establishments Acts, overtime rates varied considerably by sector and state. That variation no longer exists.

If your company operates extended working hours, shift-based roles, or project-driven overtime, your current overtime payment structure needs to be reviewed against this uniform requirement, particularly if your rates were set under a state act that previously allowed a lower threshold.

Most payroll structures we audit show basic pay at 35 to 40% of CTC. Non-compliant since 21 November 2025.

We recalculate your revised PF and gratuity liability, identify every structural gap, and give you a plan your finance team can actually implement.

Book a payroll compliance review →

How to restructure payroll without raising total CTC

Payroll compliance India restructuring does not mean raising gross salaries. In most cases, total CTC stays the same. What changes is the internal split between basic salary and allowances. Here is the structured sequence that works:

1) Run a payroll audit. Pull every employee’s current CTC breakdown and identify where basic pay falls below 50% of total CTC. The gap will vary significantly across grade levels, so flag it individually for each role.

2) Model the financial impact before changing anything. Calculate revised employer PF contributions, updated gratuity liability, and the change in employee take-home pay. Surprises during implementation create complaints and formal grievances.

3) Update employment agreements. The revised salary structure must be documented in a salary revision letter or updated appointment letter signed by the employee. System-only changes are not legally sufficient. Our employment agreements are updated for 2026 and ready to use.

4) Communicate with employees before the change takes effect. Explain clearly why take-home pay may reduce slightly and what the long-term benefit to their PF corpus and gratuity entitlement looks like. This is an employee relations step, not a formality. For guidance on keeping your broader HR policies aligned during this transition, the top 10 HR policies guide is a useful reference.

5) Update your payroll software. Ensure PF, ESI, gratuity, and overtime are all calculating on the revised wage base. Run one parallel payroll cycle before going live to catch calculation errors before they appear on official payslips.

6) Rebuild your FnF workflow. Map every step of your exit settlement process against the two-working-day requirement. Our labour law handbooks covering the EPF Act and Payment of Gratuity Act give you the statutory reference points to do this accurately.

The deduction cap most finance teams have not configured for

Beyond the wages definition, the Code on Wages, 2019 introduces a statutory ceiling on total deductions from wages in any single wage period. All deductions combined, covering PF, advance recovery, fines, damage recovery, and every other authorised deduction, cannot exceed 50% of wages for that period.

Where combined deductions breach this threshold in a given month, the excess cannot simply be taken. It must carry forward to the next wage period, not be applied in the current one. Most payroll systems are not currently configured to track cumulative deductions against this ceiling or to flag breaches automatically. That is a configuration gap that needs to be closed now.

Key fact: Under the Code on Wages, 2019, total deductions in any single wage period cannot exceed 50% of wages. Excess must carry forward. Most payroll systems require configuration changes to enforce this, it does not happen automatically.

State rules pending: what it means for payroll compliance India now

The four Labour Codes are operative at the central level from 21 November 2025. Detailed Central Rules and most State Rules needed to fully operationalise several provisions are still being notified across states.

What this creates is a dual compliance environment. Existing central and state rules remain in force to the extent they do not conflict with the new codes. For payroll compliance in India, the provisions that are already enforceable right now are the 50% wages definition, the two-working-day FnF requirement, the 2x overtime rate, and the 50% deduction cap, all under the Code on Wages, 2019.

State-level rules remain pending for certain aspects of the OSH Code relating to working hours and some social security contribution parameters. For how leave rules sit within this parallel environment, the leave rules under new Labour Codes article covers the state-level picture clearly. Companies with multi-state operations need to track each state’s notification progress actively.

For further context on the reform, the Cyril Shroff Labour Codes guide and the ILO India employment briefing are authoritative references.

Source: DLA Piper, New Labour Codes Usher in a New Era of Compliance, January 2026

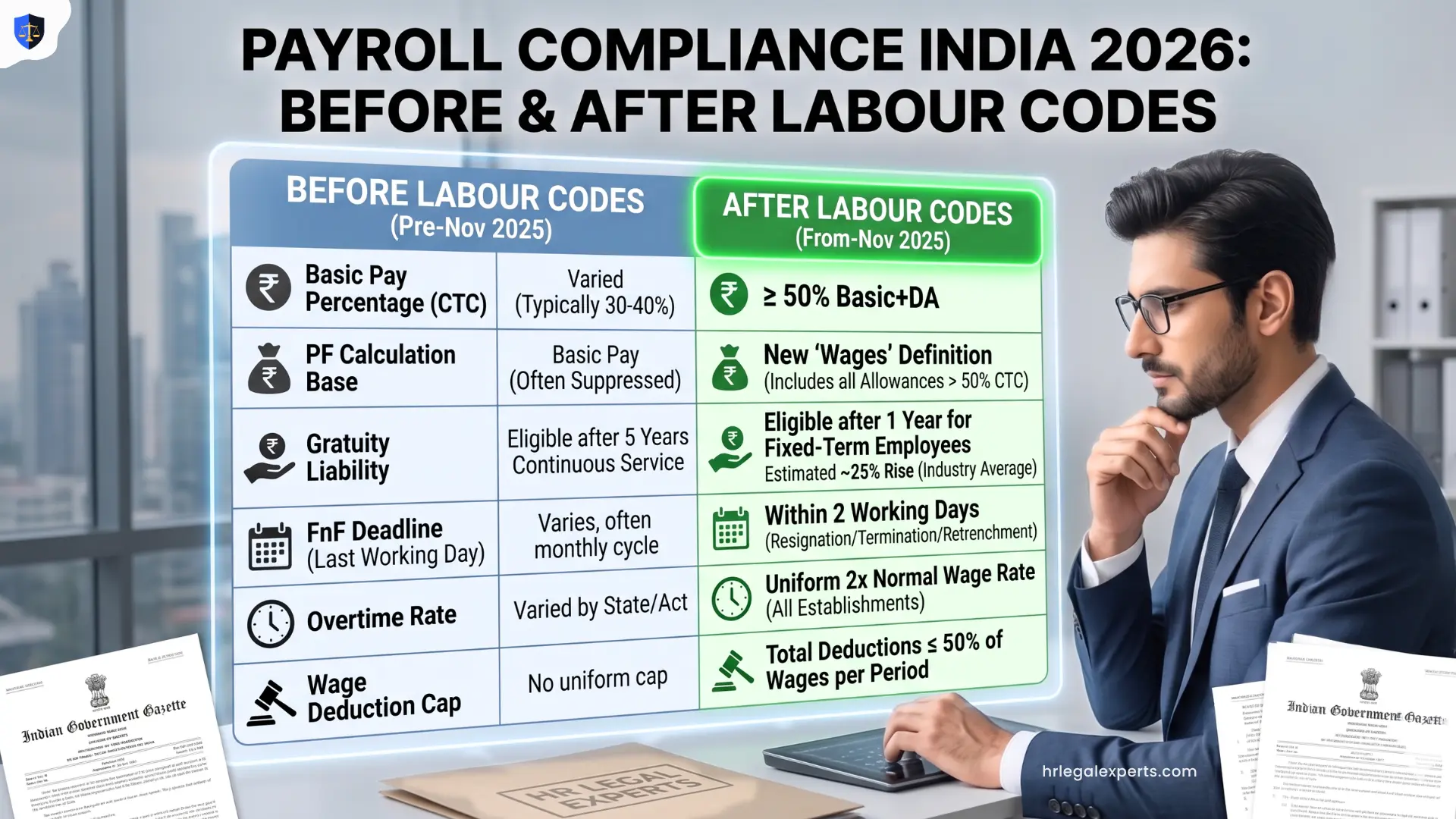

Payroll compliance India 2026: what has changed

|

Payroll area |

Before Nov 2025 |

From Nov 2025 |

|

Wages definition |

Varied by Act. No uniform rule. |

Basic plus DA must be at or above 50% of total CTC |

|

PF contribution base |

Calculated on suppressed basic pay |

Calculated on revised, higher wage base |

|

Gratuity base |

Based on lower basic salary |

Based on higher statutory wage. Estimated 25% increase in liability |

|

FnF settlement |

Typically, 30 to 45 days |

Must clear within 2 working days of last working day |

|

Overtime rate |

Varied by state and Act |

Uniform 2x normal wages across all establishments |

|

Wage deduction cap |

Varied by Act |

Total deductions cannot exceed 50% of wages per wage period |

|

Fixed-term gratuity |

Eligible after 5 years of service |

Eligible after 1 year of continuous service |

Your payroll needs a review. We do it with numbers, not just advice.

HR Legal Experts audits payroll structures for companies across India. We review CTC splits, recalculate PF and gratuity liability, test FnF workflows, and check employment documentation against the new Labour Codes. You get a prioritised action list and ready-to-use templates to implement it.

Start your payroll compliance review →

FAQs: Frequently Asked Questions

1) Does total CTC increase when restructuring under the Code on Wages, 2019?

No. In most cases, total CTC stays the same. The internal split changes: basic pay rises to 50%, allowances reduce proportionally. PF and gratuity liability increase as a result, and employee take-home may fall slightly even without a CTC increase.

2) Can employers absorb the increased PF cost to protect employee take-home pay?

Yes. Grossing up CTC to maintain existing take-home levels is a legitimate business decision under payroll compliance India requirements. It is not a statutory obligation, but it significantly reduces employee relations friction during the transition.

3) What is the penalty for not restructuring under the Code on Wages, 2019?

Non-compliance triggers underpayment of PF and gratuity, both calculated on the statutory wage base. An inspection or employee complaint can result in arrears recovery, 12% annual interest, and damages up to 100% of outstanding dues, plus fines under the Code on Wages, 2019.

4) Does the 50% wages rule apply to CXOs and senior management?

Yes. The Code on Wages, 2019 applies to all employees regardless of designation or salary level. There is no exemption for directors, CXOs, or senior management. The 50% floor covers every worker under the code.

5) Which payroll compliance India changes are enforceable right now?

The 50% wages definition, the 2-working-day FnF deadline, the 2x overtime rate, and the 50% deduction cap are all enforceable now under the Code on Wages, 2019. State-specific provisions under the OSH Code are still being notified in most states as of early 2026.

6) Where can I get a salary revision letter for CTC restructuring?

HR Legal Experts provides employment agreement and salary revision letter templates updated for 2026 payroll compliance India requirements. Access them through our recruitment templates.

2. Gratuity liability rises by an estimated 25%

Gratuity under the Payment of Gratuity Act, 1972 is calculated on last drawn basic salary plus DA. Because the Code on Wages, 2019 drives basic salary upward, every employee who has completed five years of continuous service now carries a higher gratuity entitlement than your last actuarial valuation captured.

Industry analysis estimates gratuity liabilities will rise by approximately 25% as a direct result of the 50% basic pay mandate. Beyond that, the picture has shifted further. Under the Industrial Relations Code, 2020, fixed-term employees are now entitled to proportionate gratuity after just one year of continuous service, down from the previous five-year threshold. For a detailed breakdown of how this plays out in practice, read the gratuity under new Labour Codes guide. For companies relying on contract or project-based staffing, this significantly expands total gratuity exposure.

If your last actuarial valuation was conducted before November 2025, it no longer reflects your actual liability.

Key fact: Gratuity liabilities are estimated to rise approximately 25% under the Code on Wages, 2019. Valuations done before 21 November 2025 are outdated. Fixed-term employees now add further exposure through the Industrial Relations Code, 2020, with gratuity eligibility starting at 1 year.